Free Live Masterclass · Licensed Financial Planner

What If Your Loan Repayments

Could Drop By Half.

Using The Same Income

You Have Right Now?

Discover the debt restructuring method that freed up RM 9,000 a month for Isabella, without a pay raise, side hustle, or cutting down on your lifestyle.

Because the only thing you'll lose tonight is the uncertainty about where you actually stand.

⚠️ This Session Will

Not Be Recorded. ⚠️

Ka Hoe runs this masterclass live and does not release recordings.

What is shared tonight stays in the room. If you miss it, you miss it.

Registered Financial Planner

Bank Negara & Securities Commission Malaysia

Helped clients reduce monthly repayments by 30–80% through legal debt restructuring

Maybank | UOB | Taylor's University | Community Financial Talks

Registered Financial Planner

Bank Negara & Securities Commission Malaysia

Helped clients reduce monthly repayments by 30–80% through legal debt restructuring

Maybank | UOB | Taylor's University | Community Financial Talks

This Is For You If...

This masterclass was built for one specific type of person

You earn between RM 5,000

and RM 20,000 a month but

struggle to save or invest

You have credit card debt,

personal loans, or multiple loan repayments eating into your

monthly cash flow

You have assets (property, EPF) and want to know if debt restructuring is an option for you

You want to free up

monthly cash flow so

you can actually start

building wealth

You're tired of the minimum payment cycle and want a real, structured way out

You feel like no matter how much you earn, the money is never enough

This Is For You If...

This masterclass was built for one specific type of person

You earn between RM 5,000 and RM 20,000 a month but struggle to save or invest

You have credit card debt, personal loans, or multiple loan repayments eating into your monthly cash flow

You have assets (property, EPF) and want to know if debt restructuring is an option for you

You want to free up monthly cash flow so you can actually start building wealth

You're tired of the minimum payment cycle and want a real, structured way out

You feel like no matter how much you earn, the money is never enough

This Is NOT For You If...

You are looking for a

get-rich-quick scheme or

investment tip

You are not willing to go

through a structured

evaluation process

You expect results without

any effort or document

preparation on your part

You're Not Bad With Money.

Your Structure Is

Here's what nobody tells high-income earners in Malaysia:

The more you earn, the more the bank is willing to lend you.

And the more they lend you, the more of your monthly income

gets locked into repayments before you even touch it.

It is not your fault. It is math working against a structure

you were never taught to question.

This is why you can earn RM 10,000 a month and

still feel like there is never enough.

This is why the credit card balance never seems to

go down no matter how much you pay.

This is why you keep telling yourself 'next month will be

better' and next month looks exactly the same.

You're Not Bad With Money

Your Structure Is

Here's what nobody tells high-income earners in Malaysia:

The more you earn, the more the bank is willing to lend you.

And the more they lend you, the more of your monthly income

gets locked into repayments before you even touch it.

It is not your fault. It is math working against a structure

you were never taught to question.

This is why you can earn RM 10,000 a month and

still feel like there is never enough.

This is why the credit card balance never seems to

go down no matter how much you pay.

This is why you keep telling yourself 'next month will be

better' and next month looks exactly the same.

Good Income

Full Commitments.

Nothing Left.

You've done the calculation at midnight.

Lying there, running the numbers in your head.

Trying to figure out how it all fits.

It doesn't fit.

You close your eyes and try not to think about it.

You can't tell your spouse the full picture

it would just cause a fight.

You can't tell your parents

they worked so hard to give you a better life.

You can't let your colleagues know

you're supposed to be doing well.

So you carry it alone.

And it gets heavier.

The Three Myths Keeping You Stuck

Here is why the most common approaches fail:

not because the people trying them are doing something wrong,

but because the approaches themselves are designed for a different problem

✕ Saving More

IF your credit card debt is RM 50,000 at 18% interest, THEN your annual interest

alone is RM 9,000.

IF you save RM 500 per month, THEN you're saving RM 6,000 per year.

IF interest is RM 9,000 and savings is RM 6,000, THEN your debt grows by RM 3,000 every year even when you're trying to fix it.

That's not a discipline problem.

That's a math problem.

✕ Balance Transfers

Balance transfers buy 3 to 6 months of breathing room at a lower or zero interest rate. When the promotional period ends, the full interest

rate returns often higher than before.

The debt structure never changed.

The problem returns in a different shape.

✕ Paying It Off Slowly

On RM 100,000 in debt at 18% interest, paying the minimum each month takes over 16 years and costs more than RM 100,000 in interest alone. You end up paying the original debt twice. This is the mathematics of FLIC Fixed Line Interest Calculation which most people have never been told about

None of these approaches change the structure.

The moment the structure changes,

everything else changes with it.

Because the only thing you'll lose tonight is the

uncertainty about where you actually stand.

Good Income

Full Commitments.

Nothing Left.

You've done the calculation at midnight.

Lying there, running the numbers in your head.

Trying to figure out how it all fits.

It doesn't fit.

You close your eyes and try not to think about it.

You can't tell your spouse the full picture

it would just cause a fight.

You can't tell your parents

they worked so hard to give you a better life.

You can't let your colleagues know

you're supposed to be doing well.

So you carry it alone.

And it gets heavier.

The Three Myths

Keeping You Stuck

Here is why the most common approaches fail:

not because the people trying them are doing something wrong,

but because the approaches themselves are designed for a different problem

✕ Saving More

IF your credit card debt is RM 50,000 at 18% interest, THEN your annual interest

alone is RM 9,000.

IF you save RM 500 per month, THEN you're saving RM 6,000 per year.

IF interest is RM 9,000 and savings is RM 6,000, THEN your debt grows by RM 3,000 every year even when you're trying to fix it.

That's not a discipline problem.

That's a math problem.

✕ Balance Transfers

Balance transfers buy 3 - 6 months of breathing room at a lower or zero interest rate.

When the promotional period ends, the full interest

rate returns often higher than before.

The debt structure never changed.

The problem returns in a different shape.

✕ Paying It Off Slowly

On RM 100,000 in debt at 18% interest, paying the minimum each month takes over 16 years and costs more than RM 100,000 in interest alone.

You end up paying the original debt twice.

This is the mathematics of FLIC Fixed Line Interest Calculation which most people have never been told about.

None of these approaches change the structure.

The moment the structure changes,

everything else changes with it.

Because the only thing you'll lose tonight is the

uncertainty about where you actually stand.

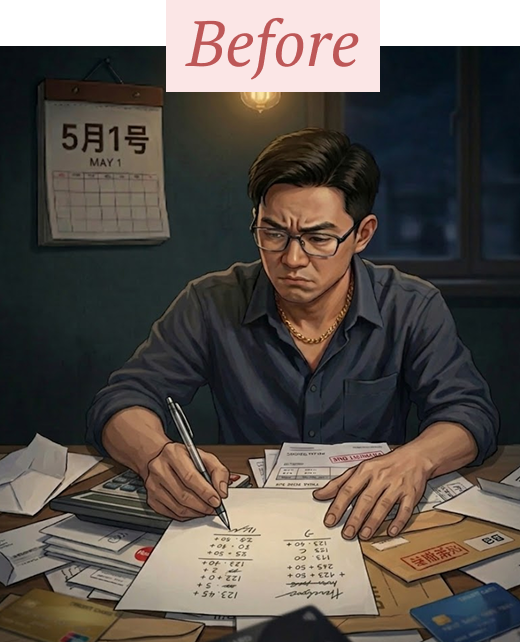

Before Tonight & After Tonight.

Right now, the first of the month

is the most stressful day.

Not because you do not earn enough.

Because by the time the commitments

are done, there is almost nothing left.

You have stopped expecting it to feel different.

This has become your normal.

You carry it quietly, manage it alone,

and tell yourself it will improve when the income goes up.

But the interest keeps running.

And the weight keeps building.

Sixty days from now, the salary comes in.

You look at the number.

And for the first time in a long time,

it feels like enough.

Not because you earned more.

Not because you cut your lifestyle.

Because the structure was fixed.

The monthly repayment is lower.

The cash flow is real.

And the thing you have been carrying alone,

you put it down.

The distance between the two is 90 minutes tonight.

Before Tonight & After Tonight

Right now, the first of the month

is the most stressful day.

Not because you do not earn enough.

Because by the time the commitments

are done, there is almost nothing left.

You have stopped expecting it to feel different.

This has become your normal.

You carry it quietly, manage it alone,

and tell yourself it will improve when the income goes up.

But the interest keeps running.

And the weight keeps building.

Sixty days from now, the salary comes in.

You look at the number.

And for the first time in a long time,

it feels like enough.

Not because you earned more.

Not because you cut your lifestyle.

Because the structure was fixed.

The monthly repayment is lower.

The cash flow is real.

And the thing you have been carrying alone,

you put it down.

The distance between the two is 90 minutes tonight.

In This Free Webinar,

Ka Hoe Will Show You

Not a general overview. A specific picture of your own financial

structure built from your own numbers, in real time.

You will leave tonight with a diagnosis ,not a to-do list.

Because the only thing you'll lose tonight is the

uncertainty about where you actually stand.

In This Free Webinar,

Ka Hoe Will Show You

Not a general overview. A specific picture of your own financial structure built from your own numbers, in real time.

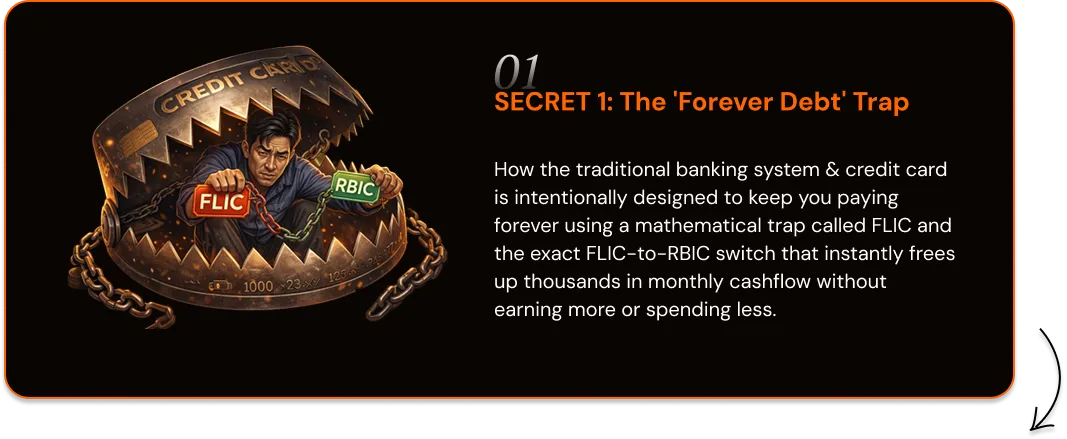

SECRET 1: The 'Forever Debt' Trap

How the traditional banking system & credit card is intentionally designed to keep you paying forever using a mathematical trap called FLIC and the exact FLIC-to-RBIC switch that instantly frees up thousands in monthly cashflow without earning more or spending less.

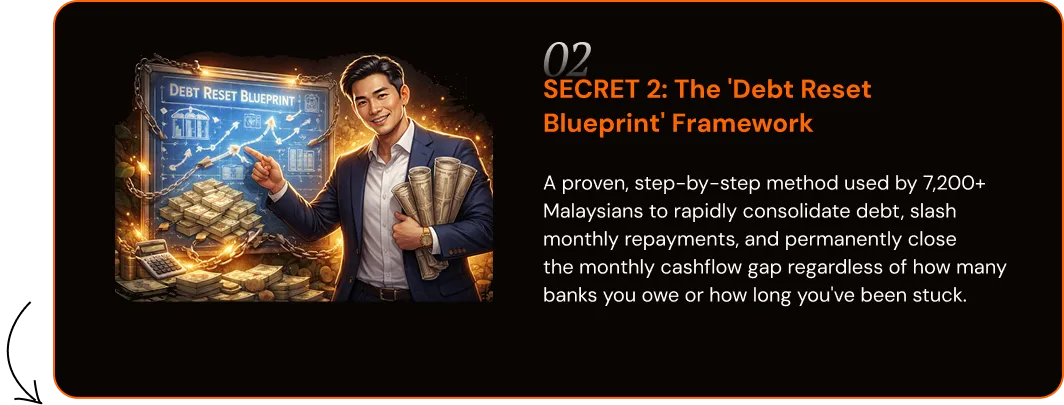

SECRET 2: The 'Debt Reset Blueprint' Framework

A proven, step-by-step method used by 7,200+ Malaysians to rapidly consolidate debt, slash monthly repayments, and permanently close

the monthly cashflow gap regardless of how many banks you owe or how long you've been stuck.

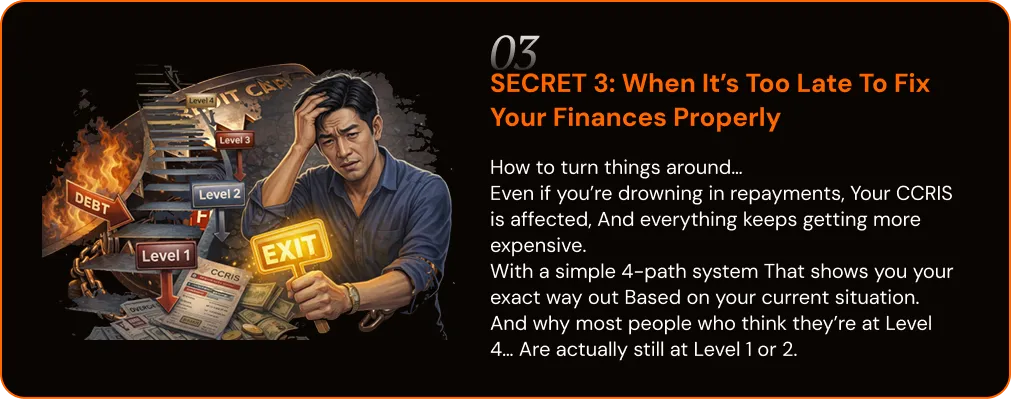

When It’s Too Late To Fix Your Finances Properly

How to turn things around…

Even if you’re drowning in multiple bank repayments Your CCRIS already has issues And the cost of living just keeps climbing

Using a simple 4-path system That shows you the right way out based on where you actually stand today

And why most people who think they’re at Level 4… Are actually still stuck at Level 1 or 2

You will leave tonight with a diagnosis, not a to-do list.

Because the only thing you'll lose tonight is the

uncertainty about where you actually stand.

He Did Not Learn This From A Textbook.

He Learned It From His Own Bank Statements.

Ka Hoe is a licensed financial planner registered with Bank Negara and the Securities Commission of Malaysia

one of the few people in this space legally

authorised to use the title.

But his authority does not just come from his license.

It comes from having lived through three financial crises

of his own including a period where he was carrying

over RM 40,000 a month in property loan repayments

and running a monthly deficit of RM 5,000.

He did not inherit a solution.

He built one by going back to first principles,

understanding how debt structures actually work,

and developing a repeatable system that he has now

used to help thousands of Malaysians.

He Did Not Learn This From A Textbook.

He Learned It From His Own Bank Statements.

Ka Hoe is a licensed financial planner registered with Bank Negara and the Securities Commission of Malaysia

one of the few people in this space legally

authorised to use the title.

But his authority does not just come from his license.

It comes from having lived through three financial crises

of his own — including a period where he was carrying

over RM 40,000 a month in property loan repayments

and running a monthly deficit of RM 5,000.

He did not inherit a solution.

He built one by going back to first principles,

understanding how debt structures actually work,

and developing a repeatable system that he has now

used to help thousands of Malaysians.

From RM 11,600/Month To

RM 2,500/Month In 60 Days

Isabella is a senior manager at a bank. Monthly income: RM 27,643. Seven children at home. Twenty staff at work. She came to Ka Hoe after years of wondering why her credit card balance never went down.

She had four credit cards, two personal loans, and multiple property loans. Every month she was paying RM 11,600 just in loan repayments. She was in deficit. She was using her EPF savings just to survive.

After working through Ka Hoe's 3-Step Debt Leverage System, her monthly repayment dropped to RM 2,500. Her total interest paid — despite the longer loan period — was actually RM 16,000 lower than before.

The night it was done, she told Ka Hoe: "Tonight I'm going to sleep so well." It was the first full night of sleep she'd had in five years.

It's really about the feeling of being in control.

Not the numbers.

The feeling of being free, no need to worry anymore, isn't it?

Answers To The Questions You Have

But Haven't Asked Yet.

Some things you might be thinking right now.

Is debt restructuring just borrowing more money?

No. Debt restructuring is reorganising the debt you already have into a different loan structure with a lower interest rate and lower monthly repayment. You are not taking on new debt — you are optimising the existing debt. In many cases, the total interest you pay over the full loan term is actually lower, even though the repayment period is longer.

I have a monthly deficit. Will the bank even approve me?

This is one of the most common misconceptions. Banks calculate loan eligibility using your Debt Service Ratio (DSR), which looks at your gross or net income against your total loan repayments — not your lifestyle expenses. High-income earners often qualify for restructuring even when they feel like they are in deficit. Ka Hoe's webinar covers exactly how this works.

I don't understand finance. Is this too complicated for me?

Ka Hoe designed his system specifically for people who have never studied finance.

The ICE JAR , Financial Compass, the IBR calculator, and the step-by-step process are all built to be used by someone with zero financial background. If you can use a phone calculator, you can follow this system.

How is this different from AKPK?

AKPK is a government programme that can take 5–10 years to complete, prevents you from taking new loans during that period, and typically negotiates interest rates of 9–13%. Ka Hoe's DCS4U (Debt Consolidation For You) can deliver restructuring in 60 days, with interest rates as low as 3–5%, and does not restrict your future borrowing. For the right candidate, the difference in total interest saved is significant.

What if Ka Hoe can't help me?

After the Debt Evaluation Session, if Ka Hoe determines he cannot help you. Whether due to your credit profile, the complexity of your situation, or any other reason. Your fee is 100% fully refunded. You only pay if he accepts your case and can deliver a solution.

Is this legal?

Yes, Ka Hoe uses a transparent, ethical and methods align to your benefits first. That means no “Ah long” , no AKPK, no faking documents and no buying prop to get more loans. He is also a Licensed Financial Planner registered with Bank Negara and Securities Commission.

You Have Been Carrying

This Long Enough

Tonight is not a sales pitch.

It is 90 minutes designed to give you one thing, clarity.

Clarity about where you actually stand.

What your options are.

And what the right next step looks like for your specific situation.

Most people leave tonight knowing more about their

own debt structure than they have known in years.

📅 Date: 19 May 2025, Monday

⏰ Time: 8:30 PM — Live on Zoom

Because the only thing you'll lose tonight is the uncertainty about where you actually stand.

From RM 11,600/Month To

RM 2,500/Month In 60 Days

Isabella is a senior manager at a bank. Monthly income: RM 27,643. Seven children at home. Twenty staff at work. She came to Ka Hoe after years of wondering why her credit card balance never went down.

She had four credit cards, two personal loans, and multiple property loans. Every month she was paying RM 11,600 just in loan repayments. She was in deficit. She was using her EPF savings just to survive.

After working through Ka Hoe's 3-Step Debt Leverage System, her monthly repayment dropped to RM 2,500. Her total interest paid — despite the longer loan period — was actually RM 16,000 lower than before.

She told Ka Hoe: "Tonight I'm going to sleep so well." It is the first full night of sleep for her after five years of dealing with debt & loan.

That’s how long she hadn’t sleep through the night.

Debt stress doesn’t come from the numbers.

It comes from not knowing what to do with them.

You Have Been Carrying

This Long Enough